Bank executives and their teams face rising customer expectations, evolving needs and behaviors, and new competitive threats — and mobile experiences are at the center of it all. The share of consumers using mobile apps for banking has spiked (overtaking online banking). Competitive pressures, meanwhile, are on the rise as disruptors roll out new capabilities and new value propositions that threaten traditional banks’ relevance and future growth.

To help banks respond to these trends, Forrester took a deep dive into a crucial question for banks: How will people’s mobile banking needs, expectations, and behaviors change in the near future? This research provides an overview of key trends, identifies 10 emerging must-have mobile features, and highlights 10 emerging differentiators in mobile banking experiences. We found that:

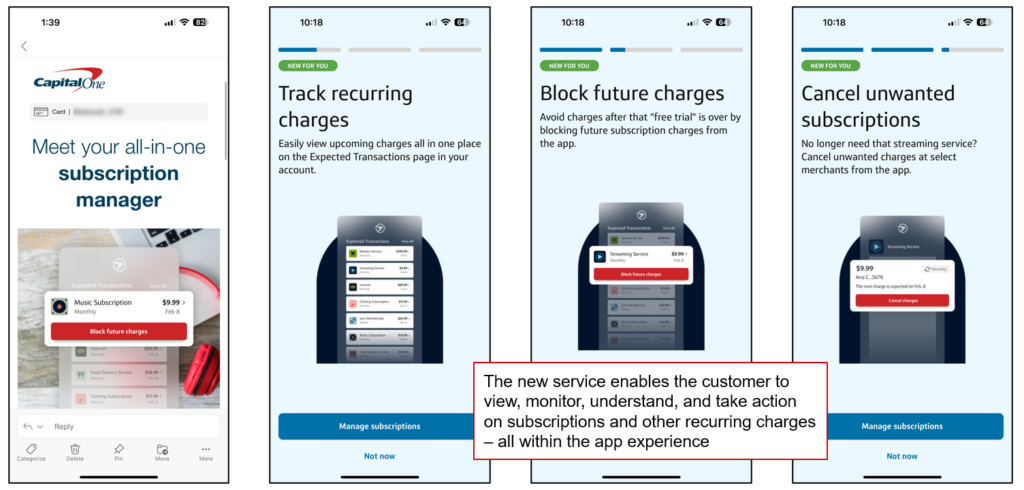

- Ten mobile banking offerings are quickly becoming table stakes. Digital leaders can no longer rightly assume that customers don’t want a full range of in-app functionality. Indeed, most US banking customers say that they should be able to accomplish any financial task through a mobile app. Our research identified 10 mobile banking offerings that are becoming must-haves. These include data aggregation, personal data management capabilities, credit builders, autonomous finance services, virtual cards, and subscription management tools (see an example from Capital One below).

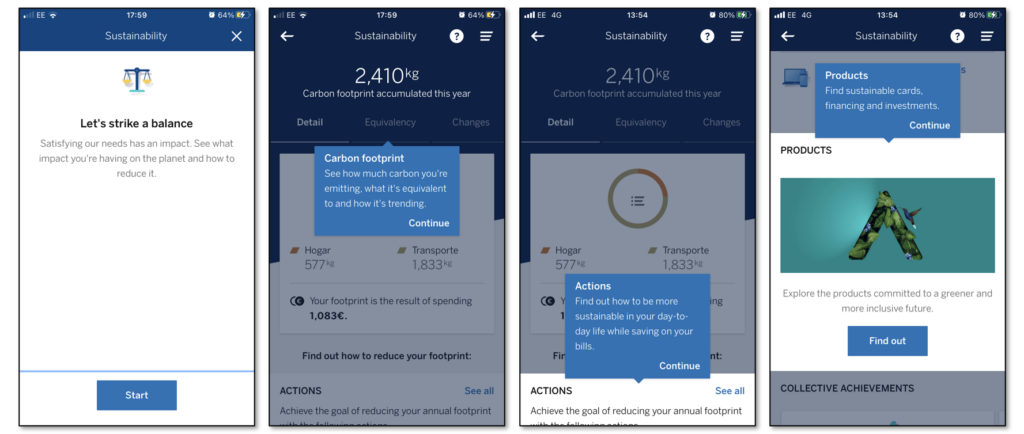

- Another 10 are emerging as brand differentiators. For most banks, the goal is not just to compete but to differentiate. To drive breakthrough growth, digital leaders should explore the products, services, features, and experiences that go beyond what people expect. Our research identified 10 differentiators, including shared finance products, international remittances and multicurrency tools, in-app search, personalized advice, charitable giving tools, and more. Often, the purpose of a given capability is not broad appeal but rather a clear value proposition to a specific audience: BBVA, for example, offers carbon tracking to attract the niche subset of green-focused consumers (see below).

- Digital banking leaders and their teams will need to ideate and prioritize. Rather than roll out every potential differentiator, digital leaders should identify and prioritize the impact of emerging, must-have offerings by customer and business objectives. Forrester’s Digital Initiatives Prioritization Tool lets digital leaders and their teams rank the relative value of different options. Digital teams should collaborate with product, business, and technology teams to explore new opportunities through experimentation, zero-base builds, and learning. Knowing what’s likely to come next will help digital banking leaders experiment with and adapt to these new features and differentiators.

Want To Know More?

If you’re a Forrester client and want to go deeper into our new “What’s Next In Mobile Banking, 2024” research, you can read our three reports:

- What’s Next In Mobile Banking, 2024: An Overview lays out the premise of our research and includes key data insights from that research.

- What’s Next In Mobile Banking, 2024: 10 Must-Have Capabilities identifies the 10 must-have mobile banking offerings for any bank looking to compete on digital experiences — including examples from firms that already offer these features or products.

- What’s Next In Mobile Banking, 2024: 10 Emerging Differentiators lays out the 10 emerging differentiators in mobile banking experiences. It also includes examples from banking brands that currently provide these offerings to customers.

If you want to discuss the full list of 10 emerging must-haves and 10 emerging differentiators, please reach out to us!

[Image 1: Capital One touts its new in-app subscription management tool for mobile banking customers]

[Image 2: BBVA calculates the customer’s carbon footprint and offers sustainable products]